Understanding Debt: The Canadian Context

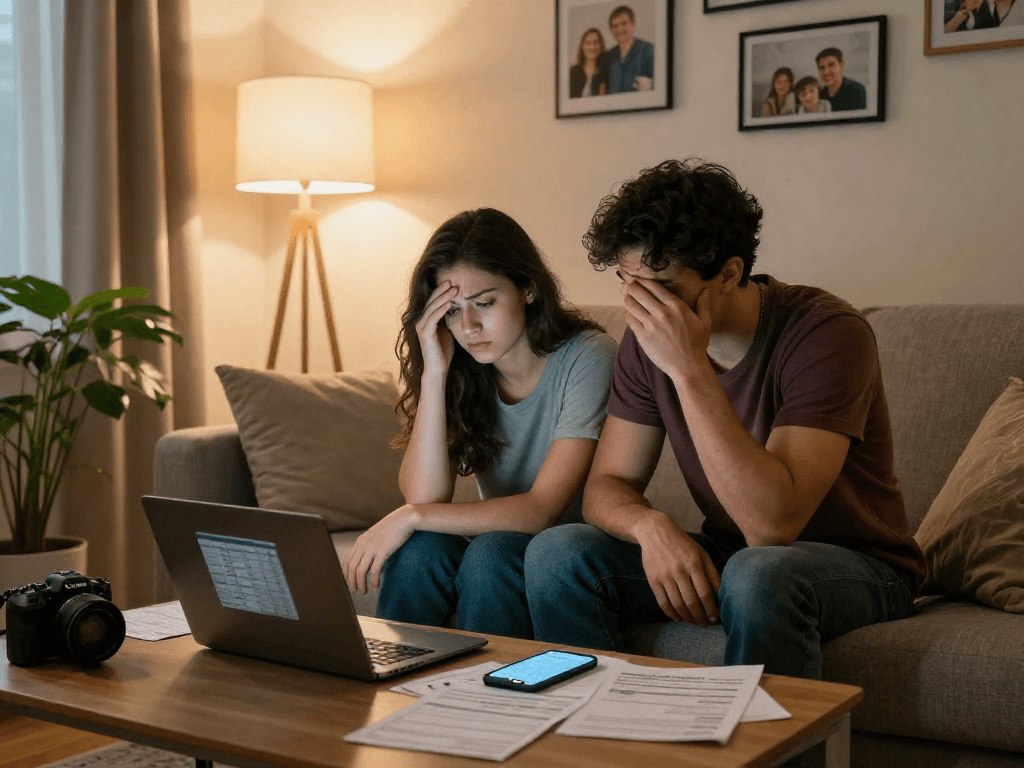

Debt is a significant issue affecting households across Canada, often leading to financial distress and emotional turmoil. Understanding the nuances of debt in the Canadian context is crucial for devising effective strategies for relief and management. With an average household debt of over $7,194 attributed to credit cards alone, many Canadians find themselves in challenging positions, seeking assistance and effective solutions to manage their finances. When exploring options, debt relief services can offer targeted strategies to regain control and improve financial health.

Overview of Debt Trends in Canada

The landscape of debt in Canada is continuously evolving, influenced by various economic factors including interest rates, housing prices, and consumer spending habits. Recent statistics indicate a surge in consumer debt levels, particularly in credit card borrowing and personal loans. A significant number of Canadians, especially millennials, are navigating these challenges as they attempt to balance student loan repayments, mortgage obligations, and everyday living expenses.

Common Types of Debt Faced by Canadians

Canadians encounter various types of debt, including:

- Credit Card Debt: Representing the most prevalent form of consumer debt, often accumulating due to high interest rates and excessive spending.

- Personal Loans: Often used for consolidating existing debts or financing large purchases, these loans can contribute significantly to a household's financial burden.

- Student Loans: These debts can affect young Canadians for years, impacting their ability to invest in homes or save for retirement.

- Mortgages: While often considered 'safe' debt, the implications of rising interest rates can make mortgage payments daunting for many.

The Emotional Impact of Debt on Households

Debt does not just affect finances; its emotional toll can be severe. Many Canadians report increased anxiety, stress, and mental health challenges associated with their financial situations. The constant worry about making payments and the fear of collection actions can lead to significant psychological impacts, including strain on family relationships and decreased overall quality of life.

Debt Consolidation: What You Need to Know

Debt consolidation can serve as a lifeline for Canadians grappling with overwhelming debt. By merging multiple debts into a single monthly payment, individuals can simplify their financial management and often secure lower interest rates.

How Debt Consolidation Works for Canadians

The process of debt consolidation involves taking out a single loan to pay off multiple existing debts. This approach can lead to lower monthly payments and reduced overall interest rates. Often, financial counselors or management firms negotiate with creditors to establish more manageable terms. These professionals play a pivotal role in helping individuals navigate the complexities of their debt situations.

Benefits of Using Debt Consolidation Services

Some key benefits of debt consolidation include:

- Simplified Payments: A single monthly payment is easier to manage compared to juggling multiple debts.

- Lower Interest Rates: Consolidation often leads to lower interest rates, reducing total debt costs over time.

- Improved Credit Ratings: A successful consolidation can positively impact credit scores as debts are paid off more efficiently.

- Reduction of Stress: Knowing there’s a structured plan in place can significantly reduce anxiety related to mounting debts.

Potential Risks of Debt Consolidation

While debt consolidation offers numerous benefits, it is essential for Canadians to be aware of potential risks such as:

- Longer Payoff Periods: Some consolidation loans extend the time needed to pay off debts, possibly leading to higher interest accrued over time.

- Unsecured to Secured Debt Transition: Turning unsecured debts into a secured loan can place assets at risk if payments are missed.

- Dependency on Budget Management: Poor budgeting practices can result in continuing cycles of debt, necessitating strict financial discipline.

Choosing the Right Debt Relief Strategy

Finding the right strategy for debt relief requires careful evaluation of personal financial situations, goals, and available options. Each person’s financial landscape is unique, and tailored solutions often yield the best outcomes.

Evaluating Personal Financial Situations

Before selecting a debt relief method, Canadians should undertake a thorough evaluation of their finances, including income, total debt, expenses, and credit ratings. This assessment forms the foundation upon which effective strategies are built.

Comparing Debt Relief Options: Pros and Cons

Canadians can choose from various debt relief options including:

- Debt Management Plans: Structured repayment plans typically involving a credit counseling agency.

- Debt Settlement: Negotiating to reduce the overall debt amount, though this can severely impact credit ratings.

- Bankruptcy: A last resort option that provides a fresh start but comes with long-term consequences.

Each approach has its benefits and potential drawbacks, making it essential to consider personal circumstances when making a choice.

Finding Trusted Credit Counselling Services

For many Canadians, engaging with a reputable credit counseling service can be a transformative step toward financial stability. When selecting a service, look for:

- Accreditation by a recognized agency.

- Transparent pricing structures without hidden fees.

- Positive reviews and proven track records of successful client outcomes.

Best Practices for Managing Debt in 2026

In an ever-changing financial landscape, staying informed about best practices for debt management is crucial. As we move through 2026, Canadians must adopt strategies that promote sustainable financial health.

Effective Budgeting Techniques to Reduce Debt

Creating and adhering to a comprehensive budget is vital for managing debt. Techniques such as the 50/30/20 rule can help individuals allocate their income effectively:

- 50% for needs (housing, groceries, bills)

- 30% for wants (entertainment, dining out)

- 20% for savings and debt repayment

Creating a Sustainable Debt Repayment Plan

A well-structured repayment plan can make a significant difference in achieving financial freedom. Prioritizing debts from highest to lowest interest rates or utilizing the snowball method (paying off the smallest debts first) are effective strategies.

Utilizing Financial Tools and Resources

There are numerous financial tools and resources available to aid in debt management, including mobile apps for tracking expenses, online budgeting templates, and financial advisors who can provide personalized guidance.

Future Trends in Debt Management

As technology evolves and the economic landscape shifts, debt management strategies must adapt to new realities. Recognizing these trends can help Canadians prepare for future financial challenges.

How Technology is Changing Debt Relief Options

Technological advancements are paving the way for innovative debt relief solutions. Online platforms and mobile apps allow users to access resources, connect with credit counselors, and manage their debts more efficiently than ever.

Predictions for Debt Trends in the Coming Years

Experts predict that rising interest rates may continue to pressure Canadian households, potentially leading to increased demand for debt consolidation and counseling services. Economic factors such as inflation and housing market fluctuations will also shape borrowing behaviors.

Preparing for Economic Shifts and Debt Challenges

As markets fluctuate, Canadians must be proactive in their financial planning. This includes building emergency funds, maintaining an adaptable budget, and staying informed about changing interest rates and lending policies.

What are the first steps to take for debt relief?

Start by evaluating your financial situation, understanding your debts, and considering options like credit counseling or debt consolidation. Creating a clear framework for managing payments will set the foundation for seeking relief.

How does debt consolidation impact credit scores?

Debt consolidation can both positively and negatively affect credit scores. Successfully managing a consolidated loan may improve your score over time, while failing to meet payment terms can lead to further declines.

Are there any hidden fees in debt relief services?

It's crucial to thoroughly research debt relief services to identify potential hidden fees. Transparent services will outline all costs upfront, allowing for informed decision-making.

What should I know before signing a debt agreement?

Before entering a debt agreement, ensure you fully understand the terms, total costs, and potential impacts on your credit. Consulting with a financial advisor or credit counselor can help clarify these details.

How can I rebuild my credit after debt consolidation?

Post-consolidation, focus on making timely payments, reducing overall debt levels, and maintaining low credit utilization. Over time, these practices will contribute to rebuilding your creditworthiness.